Blog Post

Standardizing Sustainability: The EET Explained

As the European Union tightens its regulatory framework around sustainable finance, asset managers are increasingly required to disclose Environmental, Social, and Governance (ESG) information.1 The European ESG Template (EET) is a key tool for meeting these obligations, particularly under the Sustainable Finance Disclosure Regulation (SFDR), which mandates the disclosure of sustainability risks and the integration of ESG factors into investment strategies.2

The Finance Data Exchange Working Group (FinDatEx) has been developing the EET since 2021. This group is composed of more than 80 different representatives of European interest groups, fund companies, banks, and insurance companies.3 The development was motivated by a series of EU regulations on sustainable finance that require the disclosure and exchange of ESG-related data. The contents and structure of the template were discussed in detail and were the subject of numerous feedback rounds. They reflect the current regulatory situation and market needs.

The EET is aligned with the EU Taxonomy, which the EU introduced in 2020 as a key tool of the sustainable finance framework.4 The EU Taxonomy guides financial and non-financial companies to make informed decisions and helps to direct investments towards sustainable ventures.

There is growing demand from Financial Market Participants (FMPs) for transparent, comparable, and reliable ESG data.5 The EET provides a clear and consistent format for reporting on ESG factors. This facilitates the identification of both financial and non-financial risks related to ESG issues, such as climate change, labour rights violations, and corporate governance failings, factors that are increasingly critical to identifying and managing long-term investment risks.6

Who should complete the EET?

The EET is primarily aimed at asset managers and investment firms operating within the EU or targeting EU investors. Firms that offer financial products such as investment funds, pension schemes, and insurance-based investment products can complete the template in conjunction with the SFDR and other EU regulations, to facilitate easier data exchange.

The goal of the EET is to create a machine-readable format that streamlines the collection of sustainability and ESG-related data from financial product manufacturers. The template makes the ESG data exchange process between financial market participants simpler and empowers greater accuracy in explaining a fund’s characteristics.7 It allows for the exchange of information between distributors, advisors, and other market participants to support compliance with regulatory requirements.

Sustainability disclosure applies to firms meeting certain thresholds, which may vary depending on the size of the organisation and the nature of the financial products offered. In addition, other FMPs, including institutional investors, insurers, and banks, may also need to provide ESG disclosures in line with the template, especially if they manage investment portfolios or provide sustainability-related products.8

What is included in the EET?

While earlier versions focused on the core SFDR and EU Taxonomy requirements, the current EET v1.1.3 (published December 2024 for July 2025 implementation) incorporates critical new regulatory layers, including the European Securities and Markets Authority (ESMA) guidelines on fund naming and Paris-Aligned Benchmark (PAB) compliance.

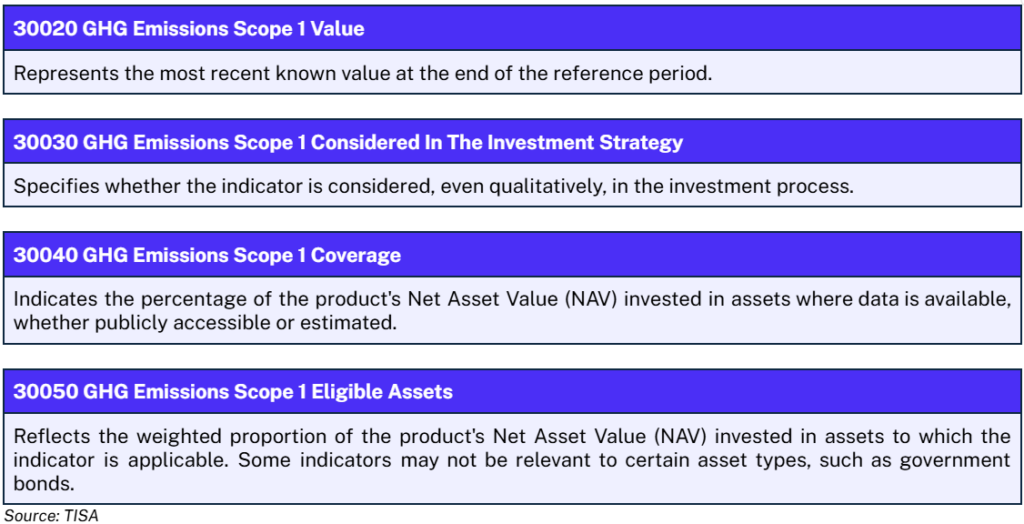

The structure of the EET is set out so that for each of the ESG indicator values included, there are three accompanying fields. This includes whether the record is considered in the product’s investment process, if there is available data (coverage) for this record, and whether this record is an eligible asset type. For example, the four key data points for Scope 1 GHG Emissions, following the pattern of each indicator, are broken down below:9

At a high level, the completion of the EET varies depending on the SFDR Article classification of the fund. The sections below outline which Article classifications fall within the scope of the EET. Where an entity manages multiple funds, a separate EET file must be produced for each financial product.10

- Article 6: All funds are classed under Article 6 if the criteria for Article 8 or 9 funds are not met. This classification implies there is no specific ESG focus on the underlying business. It nevertheless requires FMPs to disclose the integration of sustainability risks into investment decisions, alongside the likely impacts of the risks on the financial returns.11

- Article 8: Article 8 funds must follow good governance policies and promote environmental and/or social characteristics. The fund promotion can encompass claims, information, reports, and other related materials that portfolio assets are considered to have environmental or social characteristics.

- Article 9: Article 9 funds have a sustainable investment objective and must disclose how that objective is attained. It also requires information on how the sustainability objective will be attained. Also, if the objective includes a carbon emissions reduction target, it must be in line with the Paris Agreement objective.12

- ESMA Naming Compliance: Any fund using terms such as “Environmental,” “Social,” or “Impact” in its name must use the EET to demonstrate the 80% minimum investment threshold required by ESMA to avoid greenwashing.13

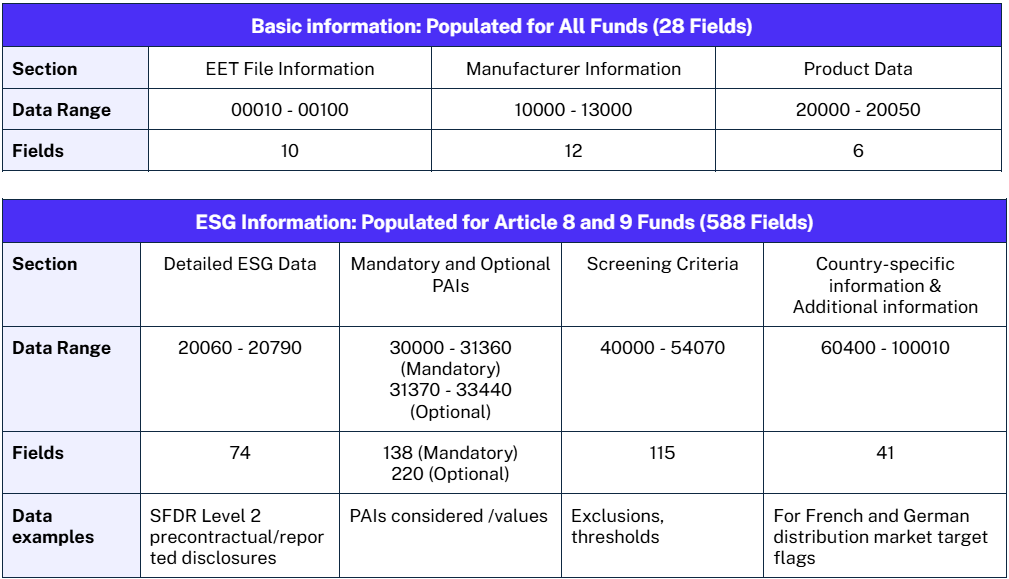

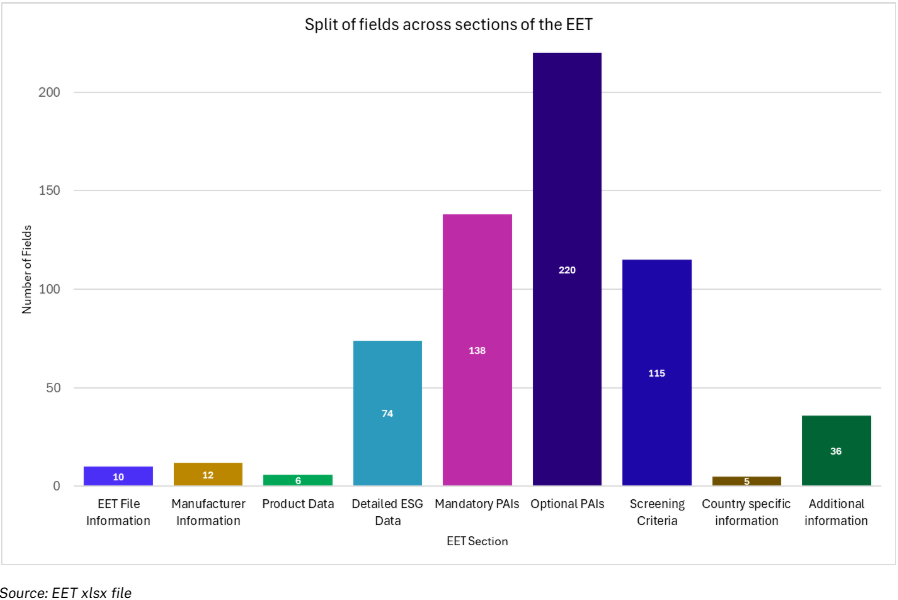

The EET v1.1.3 allows funds to report on up to 616 pre-defined data fields at a share class ISIN level; ISIN is used because there is no common identifier at the fund level. There are 30 data points required for all funds (i.e. Article 6), while detailed ESG information for the remaining data points is only completed by funds classified under Articles 8 and 9. A breakdown of the EET sections, field types, and examples of data fields within each section is given below.14 Outlined in the table below, the ‘Data Range’ refers to the unique code identifiers for each of the fields, or columns, in the EET.

The graph below shows a high-level breakdown of the field split across the different sections of the EET. As shown, the majority of the fields are related to the Mandatory and Optional PAIs, accounting for almost 55% of the total number of fields. The next largest section is the Screening Criteria, which relates to the EU Taxonomy alignment screening.

Octus Sustainability 360 Coverage

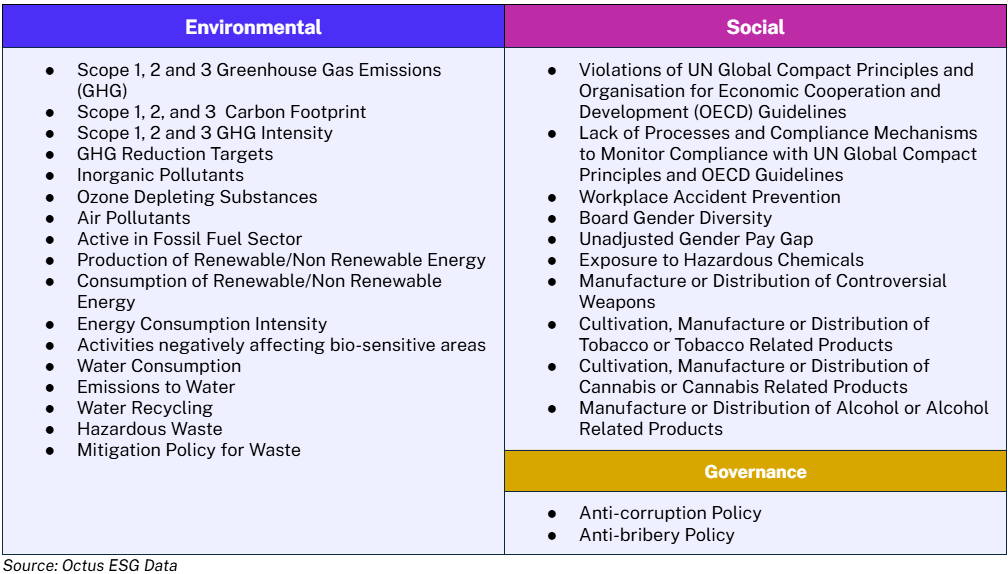

By leveraging the data from the ESG Platform, Octus can provide calculated data for 120 fields in the EET. The breakdown of key ESG indicators that feed into the EET fields can be seen below.

Stay up to date on ESG trends and data with Octus® Sustainability 360.

Resources

For further reading or to view more resources relating to the EET, please see the links below.

- FinDatEx: News and updates to the EET and the latest template.

- Template Download: European ESG Template (EET) Version 1.1.3

- FinDatEx: Webinar Recordings

- ESMA Guidelines on funds’ names: ESMA34-1592494965-657

Sources

1 EU Commission | Overview of sustainable finance

2 EU Commission | Sustainability-related disclosure in the financial services sector

3 FinDatEx | Mission statement & objectives

4 EU Commission | EU taxonomy for sustainable activities

5 PWC | Investors demand greater clarity on ESG data: How can businesses keep up?

6 TISA | Best Practice Guide to completing the European ESG Template (EET) V1.1.2

7 Greenomy | The European ESG Template (EET) Background

8 TISA | Best Practice Guide to completing the European ESG Template (EET) V1.1.2

9 TISA | Best Practice Guide to completing the European ESG Template (EET) V1.1.2

10 Datia | European ESG Template: what is it and how to start creating one?

11 EFAMA | THE SFDR FUND MARKET

12 EU Commission | Sustainability-related disclosure in the financial services sector

13 ESMA | Guidelines on funds’ names using ESG or sustainability-related terms (ESMA341592494965-657)

14 TISA | Best Practice Guide to completing the European ESG Template (EET) V1.1.2

This publication has been prepared by Octus Intelligence, Inc. or one of its affiliates (collectively, "Octus") and is being provided to the recipient in connection with a subscription to one or more Octus products. Recipient’s use of the Octus platform is subject to Octus Terms of Use or the user agreement pursuant to which the recipient has access to the platform (the “Applicable Terms”). The recipient of this publication may not redistribute or republish any portion of the information contained herein other than with Octus express written consent or in accordance with the Applicable Terms. The information in this publication is for general informational purposes only and should not be construed as legal, investment, accounting or other professional advice on any subject matter or as a substitute for such advice. The recipient of this publication must comply with all applicable laws, including laws regarding the purchase and sale of securities. Octus obtains information from a wide variety of sources, which it believes to be reliable, but Octus does not make any representation, warranty, or certification as to the materiality or public availability of the information in this publication or that such information is accurate, complete, comprehensive or fit for a particular purpose. Recipients must make their own decisions about investment strategies or securities mentioned in this publication. Octus and its officers, directors, partners and employees expressly disclaim all liability relating to or arising from actions taken or not taken based on any or all of the information contained in this publication. © 2026 Octus. All rights reserved. Octus(TM) and the Octus logo are trademarks of Octus Intelligence, Inc.