Blog Post

SFDR Reporting in Private Markets: An Analysis of 2025 PAI Data

By: Alina Simion

The Sustainable Finance Disclosure Regulation (SFDR) continues to shape how financial market participants, particularly those in the private markets, approach transparency and reporting on sustainability. Octus Sustainability 360 analyzed this year’s SFDR reporting, which highlighted key trends in data disclosure across various Principal Adverse Impacts (PAIs). While some areas show meaningful progress in both transparency and underlying performance, others continue to present challenges for investors navigating the private credit landscape.

GHG Emissions: Reporting Rates Strengthen, But Scope 3 Gap Persists

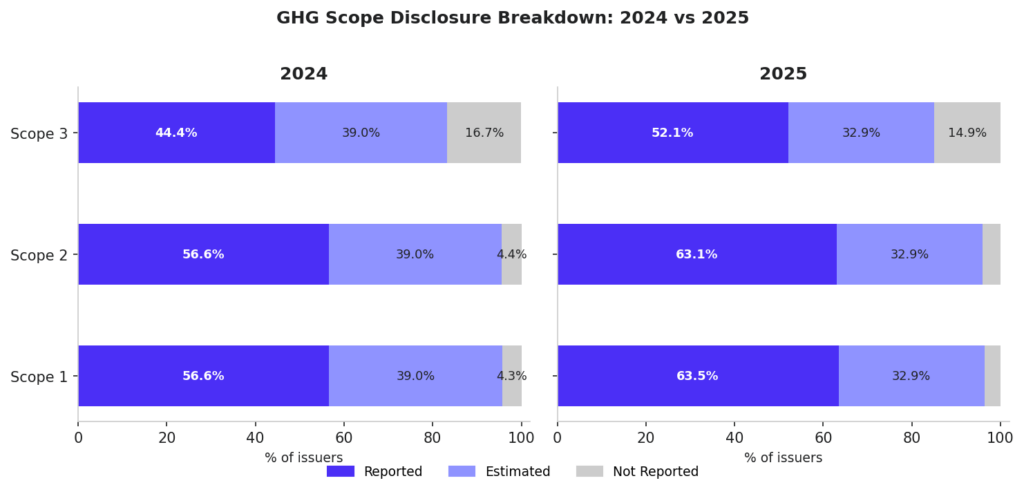

The disclosure of GHG emissions continues to present a mixed reporting landscape across Scope 1, Scope 2, and Scope 3. Scope 1 and Scope 2 emissions show a strengthening base of reported data, with over 63% of companies directly disclosing this information, up from 57% in the prior year. Scope 3, however, remains the most significant disclosure gap among the three scopes, with 15% of companies still failing to report. At the same time, progress is visible: 52% of issuers now disclose Scope 3 data, up from 44% in 2024, reflecting a continued upward trend in coverage even as absolute figures remain well below Scope 1 and 2 levels.

Figure 1: GHG scope disclosure breakdown, 2024 vs 2025

Mandatory PAIs: Broad Improvement, With Persistent Outliers

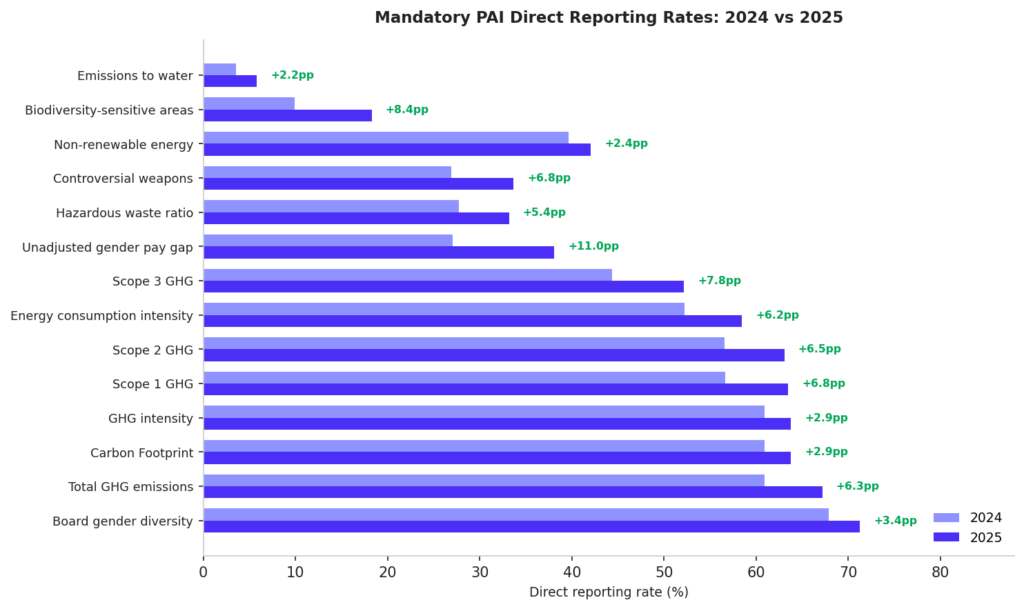

Reporting rates improved across every mandatory PAI in 2025, a consistent positive signal. The most significant gains came in indicators that have struggled for coverage in 2024. The Unadjusted gender pay gap PAI saw the largest single improvement, rising by 11 percentage points to 38% reported, though more than 60% of companies still do not disclose this data. Activities negatively affecting biodiversity-sensitive areas increased by 8.4 percentage points to 18%, and Scope 3 gained 7.8 percentage points.

Board gender diversity retained its position as the best-reported mandatory PAI, with 71% of companies disclosing directly, up 3.4 percentage points from 2024. At the other end, Emissions to water remains the weakest by a significant margin, with only 6% of companies disclosing, despite a 2.2 percentage point improvement, with 94% of companies not reporting the indicator.

It is also worth noting that two indicators, Violations of UN Global Compact principles and Organisation for Economic Cooperation and Development (OECD) Guidelines for Multinational Enterprises and Lack of processes and compliance mechanisms to monitor compliance with UN Global Compact principles and OECD Guidelines for Multinational Enterprises, are assessed entirely through ESG analyst review using company disclosures, incident records, and public information.

Figure 2: Mandatory PAI direct reporting rates by indicator, 2024 vs 2025 (percentage point change annotated)

Governance and Social Metrics: Improving Transparency, Mixed Performance

Corporate governance policy coverage improved significantly across the portfolio, with the share of investments in companies lacking anti-corruption policies falling by 40%, anti-bribery policies by 49%, and workplace accident prevention policies by 34%. These represent some of the largest year-over-year improvements across all tracked indicators and are largely attributable to increased disclosure of existing governance documentation.

Looking Ahead

The 2025 data reinforces a broader theme that has emerged across the reporting cycles: disclosure is improving steadily. Metrics that appear to deteriorate are often stabilising as more companies enter the reporting universe, while genuine improvements in policy and governance are increasingly visible. For asset managers, the priority remains active engagement with portfolio companies to close remaining disclosure gaps, particularly in environmental PAIs where non-reporting rates remain high, and to distinguish between transparency-driven data movements and real-world performance change.

Learn more about how Octus Sustainability 360 (formerly ESG Data) eases your sustainability reporting, with more than 20+ ESG reporting frameworks, including SFDR, TCFD and other global frameworks.

This publication has been prepared by Octus Intelligence, Inc. or one of its affiliates (collectively, "Octus") and is being provided to the recipient in connection with a subscription to one or more Octus products. Recipient’s use of the Octus platform is subject to Octus Terms of Use or the user agreement pursuant to which the recipient has access to the platform (the “Applicable Terms”). The recipient of this publication may not redistribute or republish any portion of the information contained herein other than with Octus express written consent or in accordance with the Applicable Terms. The information in this publication is for general informational purposes only and should not be construed as legal, investment, accounting or other professional advice on any subject matter or as a substitute for such advice. The recipient of this publication must comply with all applicable laws, including laws regarding the purchase and sale of securities. Octus obtains information from a wide variety of sources, which it believes to be reliable, but Octus does not make any representation, warranty, or certification as to the materiality or public availability of the information in this publication or that such information is accurate, complete, comprehensive or fit for a particular purpose. Recipients must make their own decisions about investment strategies or securities mentioned in this publication. Octus and its officers, directors, partners and employees expressly disclaim all liability relating to or arising from actions taken or not taken based on any or all of the information contained in this publication. © 2026 Octus. All rights reserved. Octus(TM) and the Octus logo are trademarks of Octus Intelligence, Inc.