Blog Post

Beyond sector proxies: granular activity-based screening for CLO indenture compliance

By: Scott Plumridge

Introducing Octus Activity-Based Screening

Screening in the investment space was once a blunt instrument. Simple negative filters. Binary yes-or-no calls. A list of sectors to avoid and a sign-off from compliance. That approach is no longer adequate.

As CLO indentures have grown more prescriptive and investor mandates more varied, blanket exclusions are often too broad. Effective screening is not about avoiding sin stocks. It is about identifying material involvement.

Octus Activity-Based Screening was built for exactly that distinction.

What is Octus Activity-Based Screening?

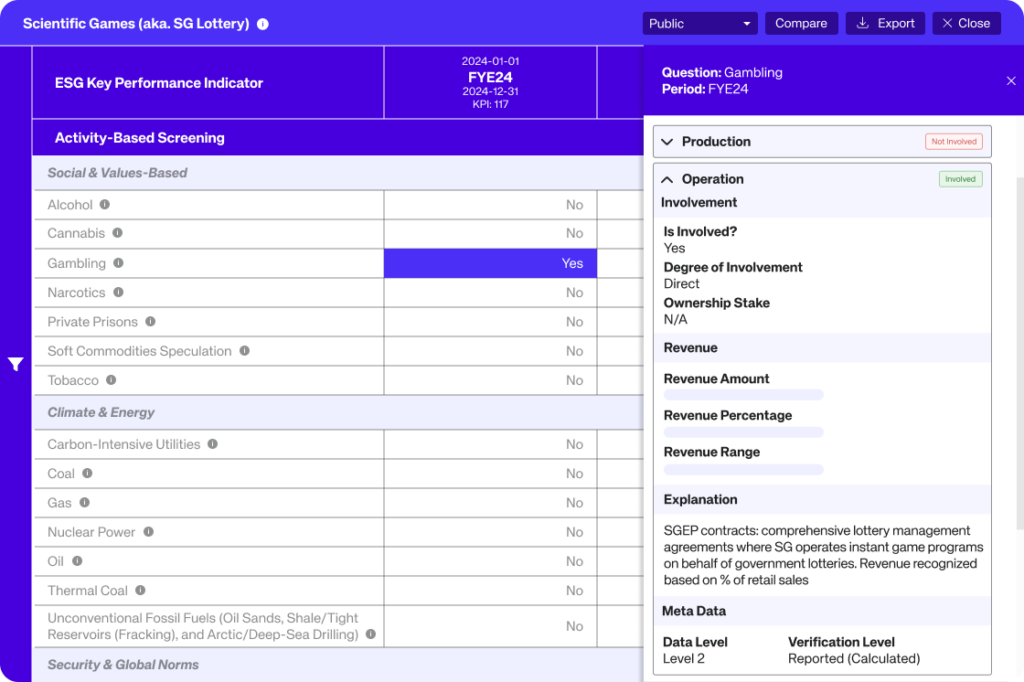

Octus Activity-Based Screening is a sophisticated credit-focused research tool designed to identify issuer-level involvement in sensitive or restricted business activities. It flags exposures that cross the most common ethical or legal thresholds identified through our research of over 500 CLO offering memorandums.

Screening across the broadly syndicated loan (BSL), high yield bond (HY) and private credit markets, Activity-Based Screening covers 30 activities, ranging from ‘Controversial Weapons’ and ‘Adult Entertainment’ to ‘Tobacco’ and ‘Biodiversity,’ to assess whether a company’s products, services or operations carry adverse reputational risks or breach specific investment mandates.

What sets Activity-Based Screening apart is granularity and private document access through FinDox™, which bridges the data gap between public and private markets. Alongside a binary yes or no, the tool identifies not only the type of involvement but also the revenue attribution. That distinction matters: it is what differentiates incidental exposure from core involvement, all within compliance boundaries. Precision at this level allows investors to make informed exclusion or active engagement decisions without unnecessarily limiting the investable universe.

Compliance

What began as occasional boilerplate language in offering memorandums has become a contractual fixture of CLO indentures: a legal prohibition that determines whether an asset qualifies as an eligible obligation. The implementation of the EU Sustainable Finance Disclosure Regulation (SFDR) in 2021 was the catalyst for ESG screening reaching the credit and private markets universe.¹ While only 15% of European CLOs included ESG screening provisions in 2018, that figure reached close to 100% of new issuance by the end of 2021 and has held there since, representing a floor rather than a ceiling.² For CLO managers, ESG screening is no longer a matter of voluntary policy or investor marketing. It is a binding structural requirement embedded in the legal architecture of the investment vehicle itself.

That shift in prevalence has been accompanied by a shift in complexity. Early indenture exclusions tended to be narrow and sector-based, targeting a small number of widely agreed harmful activities such as controversial weapons or tobacco.³ Over time the criteria have expanded in both scope and specificity: more activities, finer distinctions between types of involvement and in many cases explicit revenue thresholds that determine whether an exposure is material enough to trigger exclusion. A binary yes or no is no longer sufficient. Managers need to know the nature of the involvement and the degree to which a company’s revenues are attributable to a restricted activity.

As investor ESG mandates have grown more varied and indenture criteria more specific, the gap between broad sector filters and the issuer-level precision CLO managers actually require has widened considerably. Activity-Based Screening is built to close that gap. Delivering the granularity of involvement and revenue attribution that indentures demand, it is a credit-native screening compliance solution aligned with the proposed SFDR 2.0 and the specific exclusion criteria that govern CLO eligibility.

Granularity

The Activity-Based Screening product screens for a comprehensive range of 30 activities, organised into four thematic categories: Social and Values-Based, Climate and Energy, Defence and Global Norms, and Environmental Integrity. It identifies involvement across the entire value chain – from production and distribution to support services and commercialization. For each screen, the methodology defines what is ‘In Scope’ (primary business activity and direct exposure) and ‘Out of Scope’ (neutral infrastructure, dual-use goods or passive exposure unrelated to the core business). This ensures companies do not go undetected and are not incorrectly penalized, while giving investors the clarity needed for engagement or exclusion decisions. Each issuer-level data point is accompanied by an explanation, evidence snippet, and source disclosure, supporting auditability at every step.

To maximize precision, the tool treats specific activities as individual screens rather than grouping them. To prevent unnecessary exclusions, ‘Nuclear Weapons’ is separated from ‘Controversial Weapons’, and ‘Conventional Weapons’ is broken out into ‘Military Weapons’ and ‘Civilian Weapons.’ This level of granularity helps investors navigate the evolving responsible investment landscape.

Where involvement is identified and quantifiable, Activity-Based Screening provides the derived revenue attributed to that activity. Investors can apply materiality thresholds and make fully informed screening decisions. This depth of analysis is made possible by access to private documents – leveraging fragmented bankruptcy filings, merger agreements, spin-off prospectuses, lender presentations, meeting transcripts and term sheets to go deeper into company structures and deliver reliable revenue attribution.

CLO and Market Alignment

Activity-Based Screening was developed to meet the specific demands of CLO managers, mapping to the criteria identified through our extensive research of over 500 CLO offering memorandums and made possible by the FinDox private document universe. Through our ESG product coverage, we have access to 4,000+ global issuers, including US and European direct lending deals and 100% of the BSL and HY markets globally. The methodology’s ‘In Scope’ screening identifies the type of involvement that corresponds to the exclusion criteria defined in CLO indentures.

Our research highlighted clear market priorities. ‘Controversial Weapons’ appears in 70% of contracts. ‘Tobacco’ in 60%, ‘Adult Entertainment’ in 40% and ‘Payday Lending,’ ‘Military/Civilian Weapons’ and ‘Cannabis/Narcotics’ each appear in 35% of contracts. While these activities represent the most frequent exclusions, with high market relevance, we have integrated a broad spectrum of activities flagged in our research, including ‘Sanctions and Restricted Parties,’ ‘Ozone Depleting Substances’ and ‘Endangered Wildlife,’ to ensure comprehensive coverage across the full range of investor mandates.

Octus Activity-Based Screening moves beyond sector filters to deliver the institutional-grade, materiality-driven insights needed to align portfolios with specific values, navigate indentures and screen with confidence.

Key Capabilities

- Granular activity screening across 30 categories

- Detailed involvement scope (In Scope / Out of Scope methodology)

- Derived revenue attribution

- Private document access via FinDox

- Source disclosure and primary-source screenshots

- Detailed involvement explanation for every issuer-level data point

Sources

¹ The Historic Opportunity for CLOs Under the SFDR: The Great Leap Forward for CLOs and ESG

² European CLOs and the Unstoppable Impact of ESG

³ ESG and Euro CLOs: The Past, Present and Future

Ready to see how Octus Activity-Based Screening can sharpen your investment strategy?

This publication has been prepared by Octus Intelligence, Inc. or one of its affiliates (collectively, "Octus") and is being provided to the recipient in connection with a subscription to one or more Octus products. Recipient’s use of the Octus platform is subject to Octus Terms of Use or the user agreement pursuant to which the recipient has access to the platform (the “Applicable Terms”). The recipient of this publication may not redistribute or republish any portion of the information contained herein other than with Octus express written consent or in accordance with the Applicable Terms. The information in this publication is for general informational purposes only and should not be construed as legal, investment, accounting or other professional advice on any subject matter or as a substitute for such advice. The recipient of this publication must comply with all applicable laws, including laws regarding the purchase and sale of securities. Octus obtains information from a wide variety of sources, which it believes to be reliable, but Octus does not make any representation, warranty, or certification as to the materiality or public availability of the information in this publication or that such information is accurate, complete, comprehensive or fit for a particular purpose. Recipients must make their own decisions about investment strategies or securities mentioned in this publication. Octus and its officers, directors, partners and employees expressly disclaim all liability relating to or arising from actions taken or not taken based on any or all of the information contained in this publication. © 2026 Octus. All rights reserved. Octus(TM) and the Octus logo are trademarks of Octus Intelligence, Inc.