Case Study

BDCs on the brink? BlackRock TCP Capital Corp.

The release of Q3’25 earnings marked the moment that business development companies (BDCs) performance fully came under scrutiny, with nonaccrual loans kicking up 12% sequentially and over half of all BDCs spending more on dividend payments than cash generated.

BlackRock TCP Capital Corp., whose investment portfolio consists of positions in 149 portfolio companies with a total fair value of approximately $1.7 billion, was chief among the lot, writing down the value of their equity by 19% and trading at only 75% of adjusted book value in early 2026.

But, Octus was tracking stress within their portfolio for months ahead of the public announcement.

2025

September 11 | Q2’25 BDC Nonaccrual Analysis

Octus identified a total of $5.99 billion of debt in nonaccrual status, marking a 7% increase from Q1. BlackRock TCP issuers/borrower’s that entered nonaccrual in the second quarter included:

- 48Forty Solutions / Alpine Acquisition Corp II

- BW Holdings (Brook & Whittle)

- Fishbowl

BlackRock TCP restructuring and distressed sale activity included:

- HomeRenew Buyer

- InMoment

- SellerX

Prior to Q2, Octus identified the following BlackRock TCP portfolio companies were already in nonaccrual status:

- Gordon Brothers Finance Company

- Khoros LLC

- INH Buyer

- Razor Group

- InMoment Inc

- SellerX

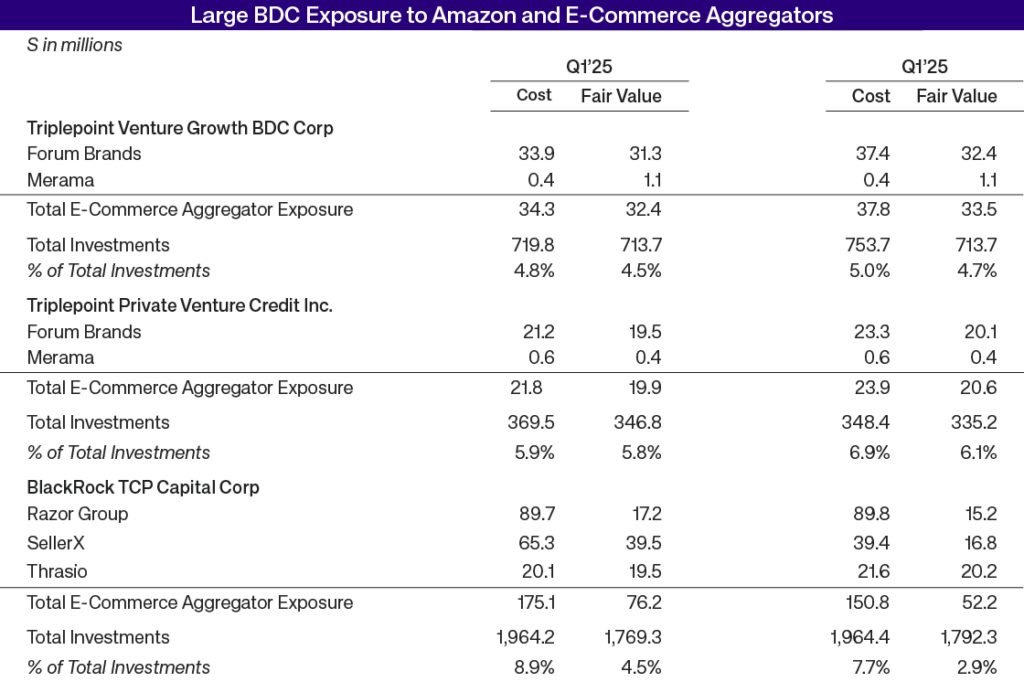

October 17 | Analysis of Amazon Aggregators Turnaround Strategies

Octus reported that, post-AWS blackout, private lenders were extending debt runways to the distressed network of third-party Amazon aggregators to right-size their balance sheets.

BlackRock TCP held a significant position in Thrasio, Razor Group and SellerX, all of which had previously reached $1B+ valuations before undergoing restructurings in late 2024 or earlier in 2025.

Although public sentiment by the companies, BlackRock TCP, or both, leaned positive, tariff-related vulnerabilities and softening consumer sentiment continued to indicate that challenges were far from over.

November 6 | HomeRenew/Renovo Liquidation Announcement

BlackRock TCP announced that HomeRenew Buyer, also known as Renovo, a direct-to-home remodeling company, began a liquidation process due to “company-specific issues,” and that it did not expect to recover value from its investment, which represented about 0.7% of its total investments at fair value as of September 30.

December 11 | Q3’25 BDC Nonaccrual Analysis

While no additional BlackRock TCP-backed loans entered nonaccrual status in the Q3’25 analysis, it was the largest BDC lender associated with the distressed sales of INH Buyer and Razor Group.

2026

January 22 | Cash-burning analysis

Octus analysis of the full universe of public and private BDCs highlighted critical stress hiding under the surface:

- More than half of all BDCs spent more on dividend payments than cash generated from portfolio assets and operating costs in the 12 months ended Sept. 30, 2025.

- Overall industry cash flow metrics improved, including lower PIK and higher cash conversion, driven by a handful of large BDCs improving metrics. However, average industry metrics worsened compared with 2024, with a larger number of funds burning cash and increasing PIK exposure.

- Average BDC net debt to net asset value increased to 0.86x. BDCs near or above 1x appeared comfortable adding debt while those materially below 1x stayed conservative.

BlackRock TCP Capital Corp. was one of the negative cash flow BDCs found, generating negative $30.3 million of cash flow after dividends in the LTM period.

January 23 | Reported Net Asset Value Decline

BlackRock TCP Capital Corp. said that it expected net asset value per share as of Dec. 31, 2025 to decline approximately 19% to approximately $7.05 to $7.09, driven by issuer-specific developments during the quarter. It also reported that debt investments on nonaccrual status would increase to 4% of fair value and approximately 9.6% at cost as of Dec. 31, compared to 3.5% and 7% as of Sept. 30, 2025, respectively.

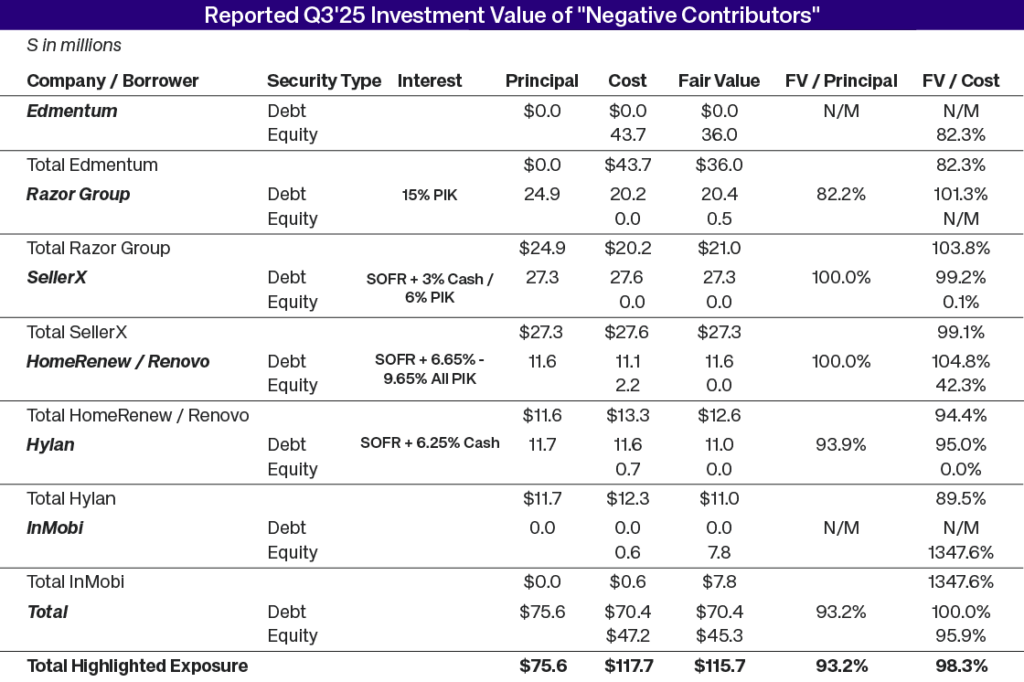

Performance detractors included familiar names SellerX, HomeRenew/Renovo and Razor, in addition to Edmentum, Hylan and InMobl.

January 27 | BlackRock TCP burning cash

Following the company’s January 23 announcement, Octus provided an analysis of BlackRock TCP’s portfolio detractors and stock performance:

Portfolio analysis:

While none of the negative contributors were on nonaccrual status as of Sept. 30, much of the affected fair value on the six negative contributors was in equity securities and a significant portion of debt securities paid interest in kind. Therefore, while the potential move to nonaccrual status for these positions would affect reported income going forward, cash income would be only marginally affected.

Additional risks identified include:

- Potential increase in its cost of debt if yields remain high or continue to climb.

- More than 20% of currently performing loans have some level of PIK component, possibly indicating an inability of borrowers to be able to fully pay interest in cash.

Stock analysis:

Within a week of the announcement, the company’s stock slide off 11%, solidifying a YoY stock decline of 44%.

February 3 | Litigation

An individual investor in BlackRock TCP Capital Corp. sued the business development company and three executives for securities fraud in the Central District of California, alleging the defendants failed to properly value the BDC’s investments and overstated its net asset value, or NAV. The plaintiff seeks certificationof a class of investors who acquired the BDC’s securities between Nov. 6, 2024, and Jan. 23, 2026.

Following the December 2025 class-action lawsuit filed against BDC manager Blue Owl in the Southern District of New York, this may signal a new era of scrutiny into BDC performance.

Representing about 25% of all direct lending activity in the United States, business development companies (BDCs) are the market’s public window into the opaque world of private credit. With Octus, you get the market-leading coverage on BDCs you need to get, and stay, ahead of the market, including:

The Market's Most Complete BDC Coverage

Representing about 25% of all direct lending activity in the United States, business development companies (BDCs) are the market’s public window into the opaque world of private credit. With Octus, you get the market-leading coverage on BDCs you need to get, and stay, ahead of the market, including:

The macro

Dedicated direct lending and BDC market analysis based on a full coverage unique of approximately 160 public and private BDCs

The micro

Dedicated news and a comprehensive data set on individual business development companies

The market signals only Octus can provide

Tap into early earmarks for direct lending distress with nonaccrual reports, fair value change analysis and restructuring transactions and recovery rates.

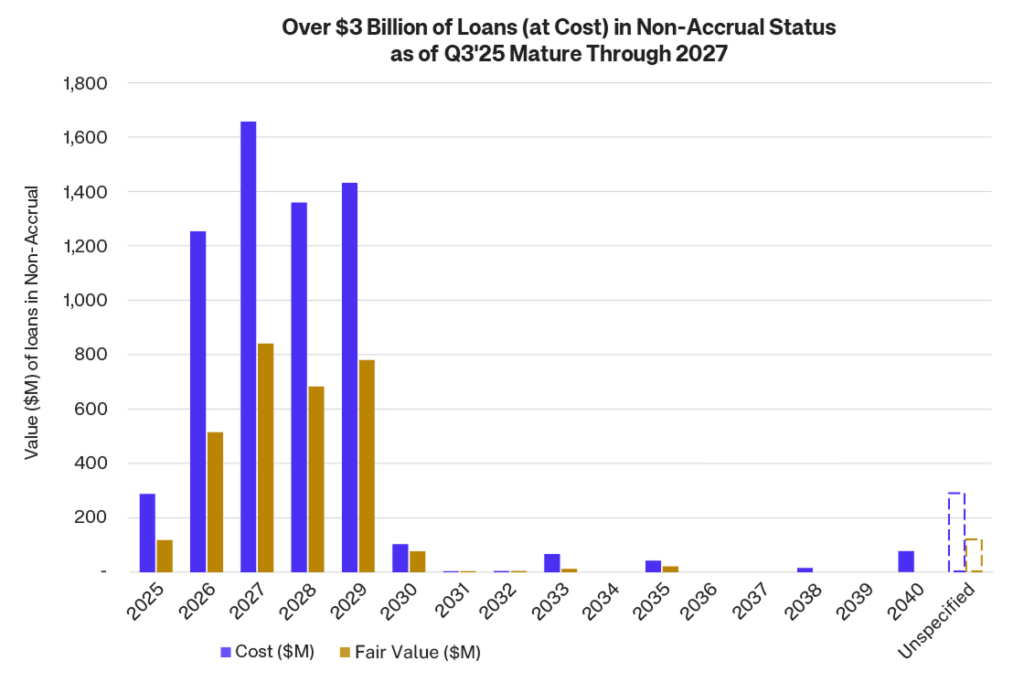

Over $3 Billion of Loans (at Cost) in Non-Accrual Status as of Q3’25 Mature Through 2027

Spot the stress before the shift.

Access the industry’s most rigorous business development company coverage and nonaccrual tracking.

This publication has been prepared by Octus Intelligence, Inc. or one of its affiliates (collectively, "Octus") and is being provided to the recipient in connection with a subscription to one or more Octus products. Recipient’s use of the Octus platform is subject to Octus Terms of Use or the user agreement pursuant to which the recipient has access to the platform (the “Applicable Terms”). The recipient of this publication may not redistribute or republish any portion of the information contained herein other than with Octus express written consent or in accordance with the Applicable Terms. The information in this publication is for general informational purposes only and should not be construed as legal, investment, accounting or other professional advice on any subject matter or as a substitute for such advice. The recipient of this publication must comply with all applicable laws, including laws regarding the purchase and sale of securities. Octus obtains information from a wide variety of sources, which it believes to be reliable, but Octus does not make any representation, warranty, or certification as to the materiality or public availability of the information in this publication or that such information is accurate, complete, comprehensive or fit for a particular purpose. Recipients must make their own decisions about investment strategies or securities mentioned in this publication. Octus and its officers, directors, partners and employees expressly disclaim all liability relating to or arising from actions taken or not taken based on any or all of the information contained in this publication. © 2026 Octus. All rights reserved. Octus(TM) and the Octus logo are trademarks of Octus Intelligence, Inc.