Case Study

PIK, Nonaccrual, Swap: The Medallia Restructuring

Thoma Bravo is set to hand over ownership of Medallia to its private credit lenders in a debt-for-equity swap that ranks among the largest private credit restructurings ever attempted. Thoma Bravo and its co-investors are staring down a roughly $5 billion loss. With $2.8 billion of debt outstanding, the lender group — led by Blackstone, with Apollo, KKR, HPS, FS KKR, Monroe and Onex also holding positions — is about to become the owner of a company it financed four years ago.

But the signals underscoring this outcome existed for months prior, tracked by Octus all along the way.

From the first quiet BDC markdown in mid-2025 to the lawyers being named in April 2026, Octus’ reporting and research teams caught every development — often before the broader market knew what was unfolding. Octus’ coverage of Medallia has provided subscribers with:

- First-to-market news from Octus’ reporting team, breaking the PIK expiry, the lender pressure campaign and the debt-for-equity swap in real time.

- BDC credit research tracking fair value markdowns across every lender in the capital structure, quarter by quarter, before the deterioration became consensus.

- Distressed analysis connecting Medallia to the broader private credit stress cycle — the maturity wall, the ARR underwriting era, and what comes next for the 2021 vintage.

Background

Medallia is a San Mateo, California-based SaaS platform that collects and analyzes customer feedback. Its Medallia Experience Cloud captures interactions across voice, video, digital, IoT, social media and corporate-messaging tools to reveal predictive insights that drive business development.

2021

July 26 | Take-private by Thoma Bravo

Thoma Bravo took Medallia private via a $6.4 billion all-cash transaction. Debt financing was provided by Blackstone Credit, Apollo Capital Management affiliates, KKR Credit, Thoma Bravo Credit and Antares Capital. The loan — over $2 billion of SOFR+650 bps term loans including 400 bps PIK, due 2028 — was originally underwritten on annual recurring revenue (ARR) rather than traditional earnings, a pandemic-era practice that had drawn increasing scrutiny as rates rose. Blackstone held the largest position at $1.5 billion, representing at least 50% of outstanding principal.

2022-2023

2022–2023 | Capital structure expands; performance targets missed

Lenders extended additional financing to fund add-on acquisitions including Mindful and Thunderhead. PIK interest accrued to principal, growing the loan balance to approximately $2.8 billion. Medallia missed performance targets that would have converted the debt into a traditional cash-paying loan — the first sign that the ARR-based underwriting thesis was under strain.

2024

2024 | Octus BDC Database catches the first cracks

Octus’ BDC Database began recording fair value markdowns across the lender group. The data told a story the market had not yet absorbed:

- Blackstone Secured Lending Fund: 98.0% of par as of Q4 2023; 94.0% by Q4 2024.

- Apollo Debt Solutions BDC: 100% of par as of Q4 2023; 86.8% by Q4 2024.

- FS KKR Capital Corp: 97.7% by Q4 2024.

- Monroe BDCs: 100.1% as of Q4 2023; 98.8% by Q4 2024.

- Onex Direct Lending BDC Fund: 99.3% as of Q4 2023; 96.2% by Q4 2024.

2025

January 7 | New CEO installed

Medallia appointed Mark Bishof as CEO, formerly chief business officer of Qualtrics, succeeding Mike Lipps, a Thoma Bravo operating partner and board member. A new leadership team was put in place to implement a turnaround plan. The sponsor stated that the issues stemmed from execution, not the structure.

August 7 | Octus reports first public markdown — sponsor still ‘supportive’

Blackstone Secured Lending Fund cut its Medallia mark to 86.7% of par, down from 89.3% at March 31, citing operating underperformance. Octus reported the markdown alongside a full lender-by-lender breakdown from its BDC Database — giving subscribers an immediate picture of who held what, and at what price, across the entire capital structure.

A source close to the matter confirmed the markdown reflected underperformance, not a loss of credit confidence. The sponsor’s equity cushion of nearly $5 billion and a conservative original loan-to-value ratio below 30% were cited as reasons lenders remained constructive. On the Q2 2025 earnings call, Blackstone management said the sponsors were “highly focused on it … They’ve been supportive.”

Octus also identified divergence across lenders that would prove meaningful later: Monroe BDCs still held at 98.5%, Onex at 96.2% — almost 10 points above Blackstone’s revised mark.

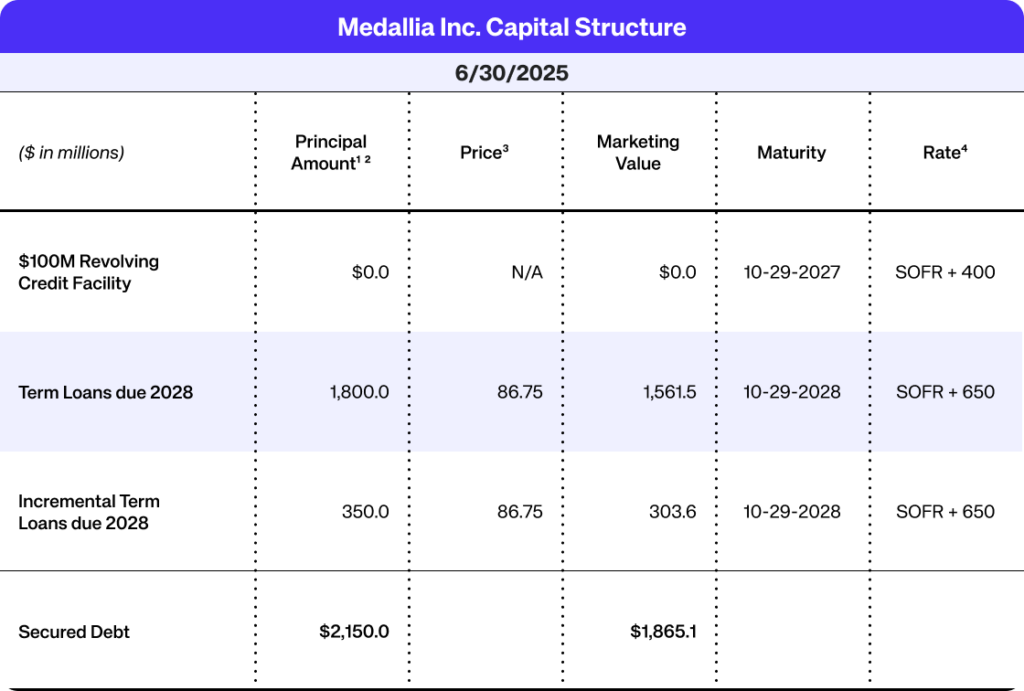

1 Unclear how much is outstanding under revolver

2 Principal amounts shown and other information based on Markit’s LoanX database

3 Pricing based on average of BDC fair value marks

4 Rate includes 400 bps of PIK interest

November 10 | Mark falls again — management calls it ‘appropriate’

Blackstone Secured Lending Fund wrote Medallia down to 82.2% of par as of September 30 — down from 86.7% at June 30 and 89.3% at March 31. On the Q3 2025 earnings call, management told investors there was “no real update from last quarter on Medallia” and the mark was “appropriate.”

Octus tracked the updated lender-by-lender marks: Monroe BDCs had fallen to 84.2%. Onex to 81.4%. FS KKR to 91.2%. The gap between the most and least bearish lenders was closing fast — downward.

The same report flagged that Snoopy BidCo, another portfolio company, had converted back to PIK from cash pay — a reminder that Medallia sat inside a broader pattern of BDC stress Octus was tracking across the market.

Q4 2025 | PIK arrangement expires; debt service exceeds earnings

A lender group led by Blackstone refused to extend further PIK relief, allowing the arrangement to expire at the end of 2025. New loan terms increased debt-servicing costs by roughly $100 million to approximately $300 million — exceeding Medallia’s annual earnings of $200 million. The company could no longer service its debt on a cash basis. The restructuring conversation was no longer hypothetical.

New loan terms increased debt-servicing costs by roughly $100 million to approximately $300 million — exceeding Medallia’s annual earnings of $200 million.

February 25 | Octus flags capital structure talks; mark implies 70% value loss

Blackstone Secured Lending Fund marked Medallia to 77.75% of par as of December 31 2025. Management stated on the Q4 2025 earnings call that the mark “implies over a 70% reduction to its setup enterprise value due to a slower-than-expected turnaround.” Thoma Bravo and co-investors had “funded over $5 billion in cash equity for this deal to date.” And for the first time, management indicated they “expect there to be discussions around the capital structure.”

Octus published the full updated mark table across all lenders. Blackstone Private Credit Fund: 85.8%. HPS: 85.0%. Apollo: 77.3%. The sponsor’s confidence narrative had cracked open.

If you are interested in accessing these fair value marks, please email [email protected]

April 2 | Private credit lenders, led by Blackstone, decline to extend PIK relief

A group of private credit lenders led by Blackstone had refused to extend further PIK relief and was increasing pressure on Thoma Bravo, according to a Bloomberg report. The path forward: either a fresh equity injection from Thoma Bravo, or a debt-for-equity swap handing control to the lenders. A swap would rank among the largest ever for a private credit loan.

Octus anchored the story with its own prior reporting: the February 25 write-down to 77.75%, the November 10 markdown to 82.2%, and the BDC Database tracking every mark in between.

April 21 | Blackstone Private Credit names Medallia as nonaccrual driver

Blackstone Private Credit Fund disclosed its Q1 2026 performance. Despite overall resilience — 97% senior secured, weighted average mark of 96.4% — the fund flagged a rise in nonaccruals to 1.4% at fair value. Medallia was named as one of only two contributors, alongside Affordable Care, with a mark of 60.3. Octus reported the update, tracking how Medallia was now a named drag on one of the largest private credit vehicles in the market.

April 22 | Octus breaks the news: Lenders set to take control, legal advisors confirmed

Octus reported that Thoma Bravo was close to handing over ownership control of Medallia to its private credit lenders by equitizing their loan holdings. With $2.8 billion of debt outstanding, it ranked among the largest private credit restructurings ever. Thoma Bravo’s equity — approximately $5.1 billion — had been impaired for a long time. Blackstone had marked down its position by more than 30%. Blackstone Private Credit Fund had moved its Medallia loans to nonaccrual status as of March 31.

Hours after breaking the story, Octus updated with the legal advisor details: Medallia is represented by Kirkland & Ellis. The private credit lender group is represented by Latham & Watkins. The two sides are moving toward a transaction in which lenders equitize a portion of their debt.

Private credit’s stress test is just beginning. The maturity wall of the 2021 vintage extends through 2028. Over $3 billion of loans currently in nonaccrual status mature through 2027 alone.

The questions Medallia’s situation is raising — when does a sponsor’s equity cushion run out, when do lenders stop extending PIK relief, what does a private credit restructuring actually look like — will be asked again, and soon.

Where are you looking to get ahead of the next Medallia?

As BDCs submit Q1 filings, here is what to watch for.

PIK and nonaccrual transitions

Octus identified 27 borrowers that switched from cash interest to deferred payments in Q4 alone. More than 250 borrowers are currently on nonaccrual. PIK is not always a precursor to distress — but when it is newly adopted on a 2021-vintage software credit, it warrants a closer look.

Lagging software marks

Q1 brought a sharp selloff in software across public equities and pricing drops across debt instruments. Octus has reported that BDCs carry more than 30% exposure to software. Where Q1 filings land relative to public market trading will matter. BDC equities are already pricing in a drop. Managers who hold marks risk a credibility gap that compounds into Q2.

Divergent fair-value marks

When multiple BDCs hold the same loan and mark it more than 5 points apart, that gap is a concern. In Medallia’s case, the divergence was visible several quarters before the restructuring. One lender held the position at 96 while another had already moved to 87.

Second extensions and quiet waivers

A second extension is typically an early sign of structural stress. The same logic applies to covenant waivers on loans that still appear performing on paper. These disclosures surface in the footnotes well before a situation becomes public knowledge.

Read more of our Private Credit coverage

Discover Octus credit market intel and data

Private Credit and Deal Origination Insights

Stay ahead with proprietary private credit and deal origination intelligence.

- Proactively source new origination or advisory opportunities

- Benchmark with data on thousands of instruments and portfolios

- Stay competitive with timely and actionable market updates

Credit Intelligence

Insights across the entire sub-investment grade universe

- Real-time credit lifecycle coverage

- Expert-backed legal and financial analysis

- Daily updates on 6,600+ companies globally

Deal Term Analytics

Enhance deal execution with instant benchmarking, clause comparison, and expert-backed insights.

- Benchmark deals and clauses in real time

- Leverage legal expertise paired with rich data

- Streamline workflows for faster, smarter decisions

This publication has been prepared by Octus Intelligence, Inc. or one of its affiliates (collectively, "Octus") and is being provided to the recipient in connection with a subscription to one or more Octus products. Recipient’s use of the Octus platform is subject to Octus Terms of Use or the user agreement pursuant to which the recipient has access to the platform (the “Applicable Terms”). The recipient of this publication may not redistribute or republish any portion of the information contained herein other than with Octus express written consent or in accordance with the Applicable Terms. The information in this publication is for general informational purposes only and should not be construed as legal, investment, accounting or other professional advice on any subject matter or as a substitute for such advice. The recipient of this publication must comply with all applicable laws, including laws regarding the purchase and sale of securities. Octus obtains information from a wide variety of sources, which it believes to be reliable, but Octus does not make any representation, warranty, or certification as to the materiality or public availability of the information in this publication or that such information is accurate, complete, comprehensive or fit for a particular purpose. Recipients must make their own decisions about investment strategies or securities mentioned in this publication. Octus and its officers, directors, partners and employees expressly disclaim all liability relating to or arising from actions taken or not taken based on any or all of the information contained in this publication. © 2026 Octus. All rights reserved. Octus(TM) and the Octus logo are trademarks of Octus Intelligence, Inc.