Case Study

First to Know, First to Report: First Brands

When it comes to rapidly evolving situations like First Brands Group, you know Octus has been breaking the latest developments and providing context and clarity with deep legal and financial research all along the way.

The full story, from every angle

Octus’ coverage of the auto suppliers’ decline has spanned nearly half a decade and, in the course of 2025 alone, has provided leading insights including:

Octus Credit Intelligence

Market-moving news from the Octus Credit Intelligence reporting team on the company’s paused refinancing efforts, advisor engagements and all the steps along the way to their September 29th Chapter 11 filing.

Private Company Analysis

Incisive financial research from our public and private financial analysts:

The Private Company Analysis team flagged the company’s substantial working capital financing, poor quality of EBITDA, and weak corporate governance—all issues that have contributed to the unravelling of the situation.

Octus Covenants Analysis

Deep legal analysis of the company’s loan documents from the Octus Covenants Analysis

All along the way, Octus’ coverage of First Brands has kept subscribers informed and moved the market. And, as the next stage of First Brands’ journey begins, know that the Octus team will be providing updates and context from the courtroom, the boardroom and beyond.

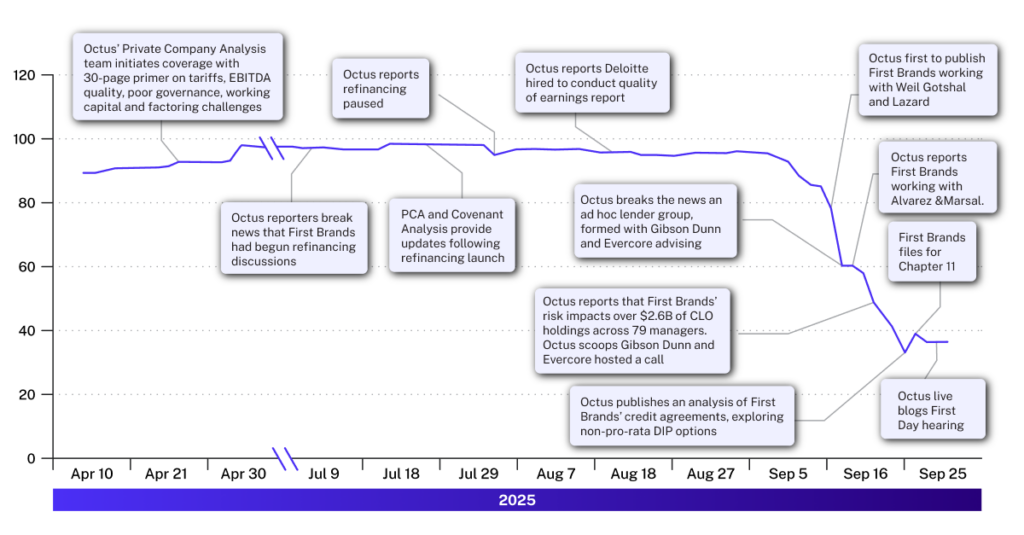

First Brands TL Price (Octus)

Background

First Brands Group is a premier automotive aftermarket platform offering comprehensive solutions for consumable maintenance and mission-critical repair parts under a portfolio of leading brands.

2022

April

In April 2022, S&P upgraded First Brands to ‘B+’ following strong 2021 outperformance, reflecting successful integration of three large acquisitions completed during 2020 and effective restructuring actions.

2023

January

In January 2023, the company launched a $250 million incremental first lien term loan for acquisitions, priced at S+500 bps with 1% floor and 96 OID, maturing March 30, 2027.

2024

March

- By March 2024, First Brands had increased total funded debt by over 60% to approximately $5 billion, with all debt exposed to floating rates.

- In March 2024, the company allocated a $525 million fungible first lien term loan at 99.25 OID and EUR225 million at 99 OID to refinance existing debt and fund the Factory Motor Parts Group acquisition.

October

In October 2024, First Brands launched additional term loan add-ons of $150 million and EUR100 million at 98 OID for future M&A and operational support.

2025

April 23 | Private Company Analysis initiation

Private Company Analysis published a deep dive 30-page primer on First Brands as loans dipped into the 80s during the liberation day sell-off.

The focus was a 360 analysis of the auto parts manufacturer and supplier with a focus on scrutiny of tariff impact. Key risks flagged included:

- Extremely heavy reliance on factoring and supply chain financing exposing the company to liquidity issues should the arrangements be withdrawn or normalized to industry levels.

- Continued poor quality of earnings with large acquisitions, “non-recurring” recurring costs, and addbacks that do not deserve to be credited according to our view. Margins significantly wide of peers also raise eyebrows. According to Octus’ analysis, “the company’s historical margins appeared significantly higher than those of publicly traded peers, which we believe may not accurately reflect the company’s true profitability because of weak corporate governance and limited transparency.”

- The Octus Private Company Analysis continued: “First Brands exhibits weak corporate governance, with the founder-CEO, Patrick James, maintaining what appears to be absolute control. There is limited to no public background and no disclosure of a board of directors or any corporate oversight from a board of directors. Without support from a financial partner, there may be limited capacity to inject additional equity if needed in a distressed situation such as a recession, a destocking cycle or the factoring lines being reduced or pulled. James may do whatever it takes to retain control, such as adding debt, dropdown transactions or selling key assets, which might be detrimental to the company’s current creditors.”

May 14 & May 22 | Private Company Analysis earnings coverage

Private Company Analysis published a memo on Q1’25 earnings and investor call of First Brands.

July 9 | Reporting on potential amend & extend

Octus reporters broke the news that First Brands had begun discussions with existing lenders about restructuring its capital. The financing, led by Jefferies, was reported to include a $2.7 billion first lien term loan, €850 million first lien term loan, and a $1 billion first lien fixed-rate tranche, with discussions on their second-lien term loan ongoing.

July 24 | Private Company Analysis, Covenant Analysis provide refinancing updates

Private Company Analysis published an update of the First Brands analysis and model following the refinancing launch. Covenants Analysis completed an analysis of the documentation for First Brands’ new loans, identifying middling borrower flexibilities and lender protections in loan documents.

August 4 | Reporting on refinancing pause

August 14 | Deloitte hired to conduct quality of earnings report

Octus reported that, after the failure to refinance resulted from investor skepticism about the company’s financial disclosures, particularly regarding its accounts receivable factoring programs. The company hired Deloitte to conduct a quality of earnings, or QoE, report to address these concerns—a red flag that suggested deeper accounting issues.

August 15 & August 29 | Private Company Analysis earnings coverage

Private Company Analysis published a memo on Q2’25 earnings and investor call of First Brands.

September 18 | Private Company Analysis publishes analysis of First Brands working capital arrangements versus the rest of the industry

Private Company Analysis published out a market update on First Brands, providing working capital benchmarking with peers, given the company’s use of factoring arrangements and the broader market concerns.

September 17-24 | Restructuring reporting

- September 17: Octus was the first to publish that First Brands was working with Weil Gotshal and Lazard to evaluate its options.

- September 18: Octus broke the news that First Brands was considering a restructuring and debating whether it would be in- or out-of-court. Additionally, Octus reported that several of their term loan lenders went restricted, an ad hoc group of lenders was being formed, with Gibson Dunn as legal advisor and Evercore as their financial advisor.

- September 19: Octus reported that First Brands was working with Alvarez & Marsal as financial advisor. After this tumultuous week, First Brands’ loan dropped significantly, from the mid-80s to the mid-50s.

- September 23: After reporting that First Brands’ restructuring risk would impact over $2.6B of CLO holdings, across 79 managers, Octus shared the scoop that advisors to First Brands Group’s lenders–Gibson Dunn and Evercore–hosted a call to discuss a debtor-in-possession loan, where lenders, including those with exposures of more than $100 million, discussed providing the loan on a pro rata basis.

- September 24: First Brands loans continued to fall, dropping into the low 40s.

September 25 | Related entities begin seeking bankruptcy protection

- Several entities related to First Brands Group filed for Chapter 11 bankruptcy in the Southern District of Texas. The bankruptcy petitions were filed by Carnaby Capital Holdings and its affiliates, all signed by First Brands Group’s founder and CEO, Patrick James. The petitions did not explicitly mention First Brands Group, but the companies share a corporate address in Cleveland and are represented by the same legal counsel, Weil Gotshal.

- Octus reported that the group of lenders reviewing First Brands Group’s capital needs expanded and were expected to bring a “nine-digit increase” in group holdings.

- First Brands’ loans were quoted as being in the high 30s.

September 26 | Analysis of potential non-pro-rata DIP

The Octus team published an analysis of First Brands’ credit agreements, exploring non-pro- rata DIP might be achieved within the bounds of their documents.

September 29 | First Brands Chapter 11 Filing

First Brands filed for Chapter 11 in the Southern District of Texas, to “stabilize its business operations and facilitate a value-maximizing transaction,” according to a press release. According to the petition, the debtors report $1 billion to $10 billion in assets and $10 billion to $50 billion in liabilities.

October 1 | First Day Hearing

Octus reported live from the courtroom for the duration of the hearing, publishing 11 articles on DIP objections, interim approvals, ad hoc holdings and adequate protection.

Discover Octus credit market intel and data

Credit Intelligence

Insights across the entire sub-investment grade universe

- Real-time credit lifecycle coverage

- Expert-backed legal and financial analysis

- Daily updates on 6,600+ companies globally

Private Company Analysis

Get in-depth research into private companies across the credit lifecycle.

- Tap into comprehensive coverage of an opaque market

- Access a robust team of analysts with decades of experience

- Obtain insights on over 250 key secondary names

Covenants Analysis

Empower your decisions with in-depth analysis on US/EU bonds and loans.

- Leverage deep data access to deal documents and reports

- Inform critical decisions with timely market insights

- Manage risks with detailed legal and financial analysis

This publication has been prepared by Octus Intelligence, Inc. or one of its affiliates (collectively, "Octus") and is being provided to the recipient in connection with a subscription to one or more Octus products. Recipient’s use of the Octus platform is subject to Octus Terms of Use or the user agreement pursuant to which the recipient has access to the platform (the “Applicable Terms”). The recipient of this publication may not redistribute or republish any portion of the information contained herein other than with Octus express written consent or in accordance with the Applicable Terms. The information in this publication is for general informational purposes only and should not be construed as legal, investment, accounting or other professional advice on any subject matter or as a substitute for such advice. The recipient of this publication must comply with all applicable laws, including laws regarding the purchase and sale of securities. Octus obtains information from a wide variety of sources, which it believes to be reliable, but Octus does not make any representation, warranty, or certification as to the materiality or public availability of the information in this publication or that such information is accurate, complete, comprehensive or fit for a particular purpose. Recipients must make their own decisions about investment strategies or securities mentioned in this publication. Octus and its officers, directors, partners and employees expressly disclaim all liability relating to or arising from actions taken or not taken based on any or all of the information contained in this publication. © 2026 Octus. All rights reserved. Octus(TM) and the Octus logo are trademarks of Octus Intelligence, Inc.